Did you know that medical debt is the most common collection type on consumer credit reports? According to the Consumer Financial Protection Bureau, medical debt made up 58% of all collections tradelines in Q1 2021. Total consumer medical debt is estimated to be anywhere from $81 billion to $140 billion, with up to 35% of American adults carrying some form of medical debt. More debt means fewer people seeking medical care, which negatively impacts everyone.

No wonder your clients and their employees are struggling to cover healthcare costs. They’re being crushed by mountains of debt that just keep accumulating. Something’s got to give.

On July 1, it finally did. That’s when an important update to the Fair Credit Reporting Act (FCRA) went into effect. Called the Medical Debt Relief Act, this update will wipe out medical debt black marks that have appeared on many consumers’ credit reports for way too long.

With this update, all three major U.S. credit bureaus—TransUnion, Equifax, and Experian—have agreed to remove $500 of medical debt from their credit reports if it’s already been paid by the consumer. So, if a person owed $499 and has already paid it, that debt will get wiped off the books and the consumer’s credit score will go up. Even better, as of the first half of next year, the three bureaus will no longer include collections of less than $500 of medical debt on consumers’ credit reports. This will positively impact up to the 70% of Americans that have a medical debt credit impairment under $500.

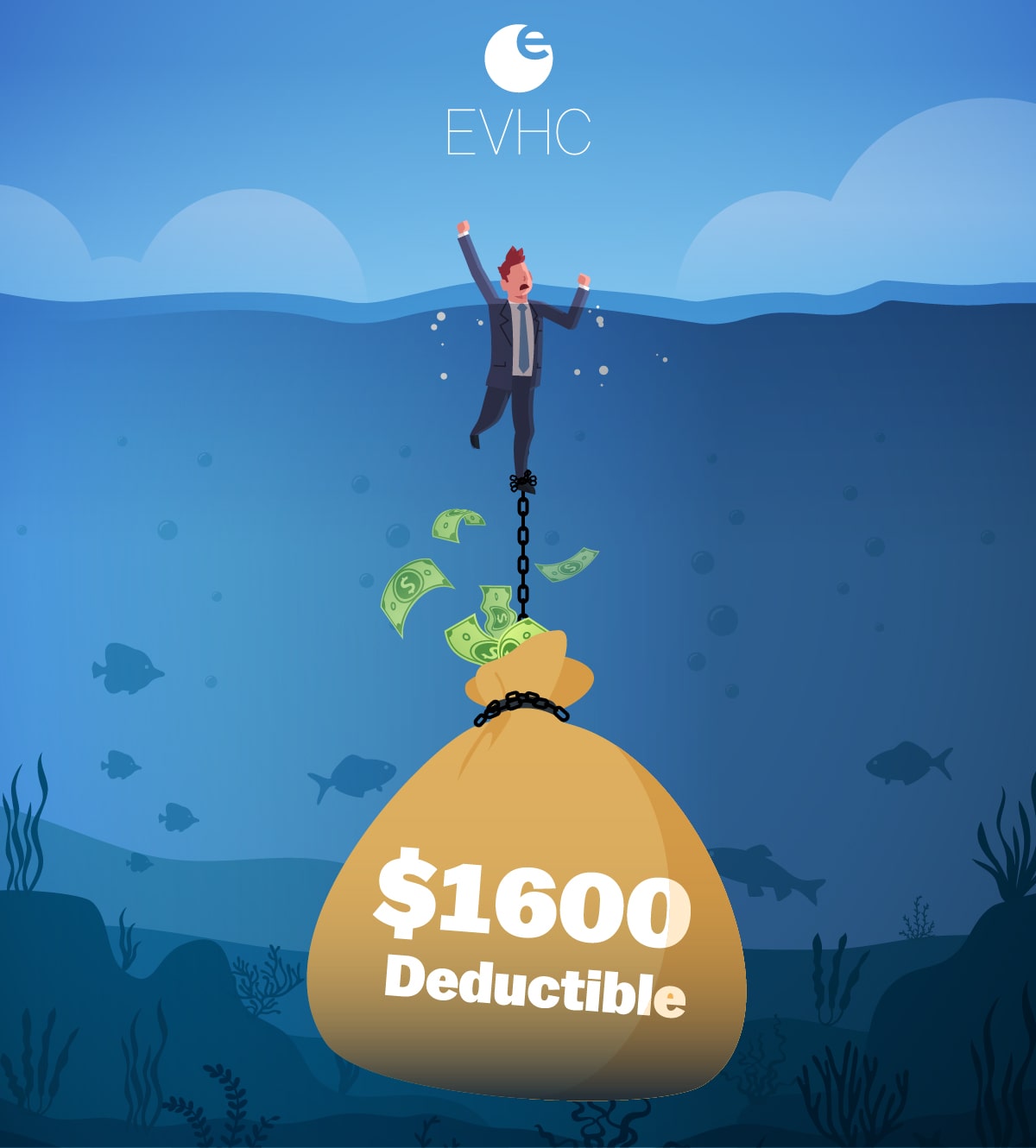

In addition, members will now have one year to contest a debt that’s gone into collections before it appears on their reports. It used to be six months. Now, consumers have double the amount of time to negotiate their outstanding bills with their providers before they get dinged on their credit reports. This is particularly huge when considering the average person has more than a $1,600 deductible (and $3,500 for families!). The update is really going to help consumers that have those high deductibles and simply cannot afford to pay their ever-increasing medical debt all at one time.

The Act is a massive boon to everyone involved, for several reasons:

The update is yet another way for employers and employees to save on healthcare costs or at least defer them without having to worry about their credit rating suffering. Along with partially self-funded insurance and reference-based pricing, it will help relieve many of the financial headaches that health insurance too often causes.

Forgiveness of medical debt is the first substantial update to the FCRA since the original Act became law in the 1970s. Along with the recent passage of the No Surprises Act, which eliminates surprise medical bills, it’s a significant leap in the right direction in terms of helping people save money on health insurance.

We need to keep this drumbeat rolling. There’s no reason to continue to put more financial pressure on the already working poor, and no reason to give CEOs, CFOs, and Chief Human Resource Officers any more reason to worry about affording top-tier medical coverage for their employees.

Let’s chat about ways we can continue to control healthcare costs, together. Contact us to learn more about how the Medical Debt Relief Act will impact you and your clients, and let’s have a conversation about how you can use the new Act to your advantage.

.png)